CD interest rates today

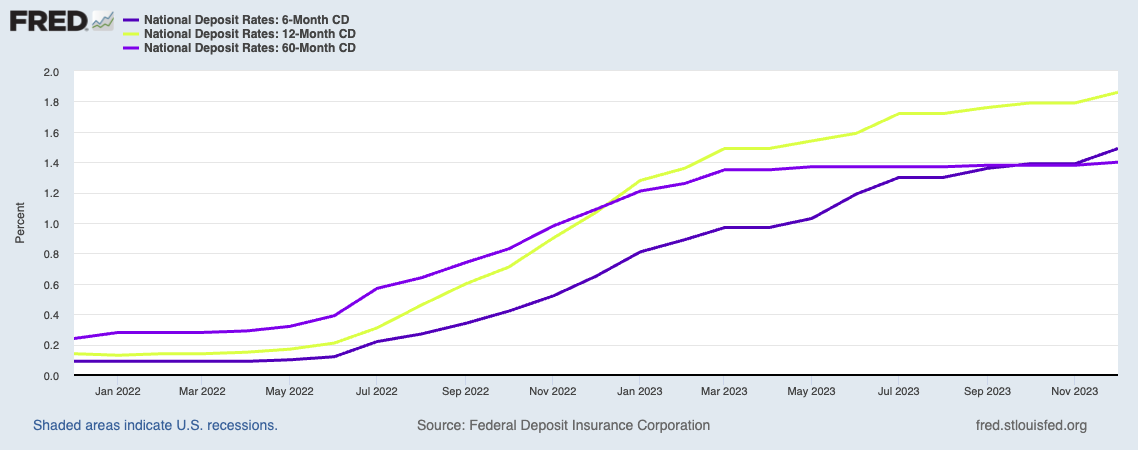

One-year CD rates have risen continuously since April 2022, after reaching a low of 0.13% average annual percentage yield (APY) in January of that year. Five-year CD rates, which were as low as 0.24% APY in December 2021, also began to rise steadily in April 2022.

As of Dec. 18, 2023, the average APY on one-year CDs was 1.86% and the average on a five-year CD was 1.40%, according to the Federal Deposit Insurance Corporation (FDIC).

Of course, these are just averages. CD rates vary between banks, and the best CD rates are above the average. You just need to know how to find them.

With the pace of rate increases slowing or coming to a halt, what will happen to CD rates in the next few months?

Ready to boost your savings?

Click here for the best savings accounts! Discover top rates and no-fee options to grow your money effortlessly.

Start saving smarter today!Why did CD rates move higher?

CD rates are correlated with the fed funds rate. If this rate rises, so will the rates on CDs, although sometimes with a lag. Typically, longer-term CDs pay higher rates than shorter-term CDs, but this is not the case right now because the yield curve is inverted, which means longer-term rates are lower than short-term rates.

Rates vary between institutions because some institutions choose to compete for savers by paying higher rates. Online banks frequently offer higher rates for this reason. Credit unions will often pay higher rates because they are non-profits. Rather than paying shareholders, they return their profits to members, and one way they might do this is through higher savings rates. At many institutions, the rate is also higher as you invest more.

The fed funds rate is the rate banks charge other banks when they lend them money overnight. The target range for this rate is set by the Federal Open Market Committee (FOMC) at the Federal Reserve, which is the central bank of the U.S. The committee meets eight times yearly to set the target rate based on economic conditions. For instance, they may raise the target rate to slow down the economy if the inflation rate is too high, or lower it to stimulate the economy if unemployment is too high.

Other interest rates, such as those on U.S. Treasurys, mortgages, loans and savings tend to move in the same direction as the fed funds rate and the best CD rates tend to average near the top of the fed funds target range.

In 2020, U.S. inflation began to rise dramatically until it peaked at 9.1% year-over-year in June 2022. To combat this inflation, the Fed raised the target fed funds rate seven times in 2022 and four times in 2023, and now the target range is 5.25% to 5.50%.

CD rates are likely at or near their peak

These rate hikes appear to be working. The inflation rate has fallen to 3.1% and FOMC members, market participants and economists believe the fed funds rate will be lowered some time this year.

The FOMC has kept rates unchanged at its last three meetings, and at the last meeting, held December 12-13, 2023, all but two of the 19 meeting participants predicted a lower target rate range in 2024, and none predicted further rate increases.

The markets are also expecting a lower fed funds target rate. According to the CME FedWatch Tool, as of Dec. 28, 2023, there’s an 88.3% probability the Fed will lower rates at least 0.25% at their March 2024 meeting and a 99.8% probability they will lower them at or before their May 2024 meeting, based on trading activity in fed fund futures.

Similarly, Bloomberg's monthly survey of economists, conducted after the December FOMC meeting, showed a median expectation that the Fed will start lowering rates in 2024, but not until the June 2024 policy meeting.

Since CD rates move with the fed funds rate, there’s a strong chance they’ll fall in 2024, and this may begin happening as soon as springtime.

Of course, no one can predict the future. In the press release that followed its most recent meeting, the FOMC acknowledged that inflation “remains elevated” and kept open the possibility that future rate hikes may be necessary to return inflation to their target of 2%.

If you believe rates might fall soon, you might consider investing in longer-term CDs to lock in higher rates. If you think CDs may go up further, and you’re worried about being locked into a low-rate CD while rates continue to rise, you should consider CDs with shorter terms to take advantage of higher APYs when they become available.

Another strategy is to build a CD ladder with short-term CDs to maintain flexibility in a rising rate environment. This means dividing your investment across multiple CDs with different maturities. With this method, you’ll have CDs maturing every year and then get regular opportunities to invest in CDs with better rates.

This 2 minute move could knock $500/year off your car insurance in 2025

OfficialCarInsurance.com lets you compare quotes from trusted brands, such as Progressive, Allstate and GEICO to make sure you're getting the best deal.

You can switch to a more affordable auto insurance option in 2 minutes by providing some information about yourself and your vehicle and choosing from their tailor-made results. Find offers as low as $29 a month.

Find the best rate for youCDs are solid investments

CDs are a more lucrative and nearly risk-free alternative to standard or high-yield savings accounts. If you’re with a bank insured by FDIC or a credit union insured by the National Credit Union Administration, your money is guaranteed up to $250,000.

If you have concerns about deciding how much to invest, you can shop around. Banks offer CDs with various terms, so you don’t have to commit to any specific timeline or sum of money.

In addition to traditional, fixed-rate CD products, there are also other types of CDs you can invest in.

Liquid CDs allow you to make withdrawals more easily and without financial penalty.

Variable CDs have interest rates that rise or fall according to some benchmark, like the Consumer Price Index, the prime rate or the performance of the S&P 500.

Bump-up CDs allow you to take advantage of rising rates by allowing a limited number of boosts to your interest during the term.

The only risk you’ll encounter is not abiding by the CD rules. For instance, if you need to withdraw your funds before the fixed term ends, you’ll likely have to pay a penalty equal to a chunk of the interest you’ve earned.

Banks offering the best CD rates

Some banks offer competitive CD rates well beyond the national average, so comparing offers is essential. Here are some of the best CD rates monitored by Moneywise:

-

Quontic Bank offers CDs with terms from six months to five years. The minimum deposit is relatively low for an online bank at $500. If you don’t want to lock your money away for long, the six-month CD still has a strong return of 4.25% APY and the one-year CD jumps down to 4.00%.

-

CIT Bank is great for those seeking a more flexible option. They offer an 11-month no-penalty CD with an APY of 3.50%. The minimum deposit is $1,000, but you can withdraw the total balance and interest earned without penalty after seven days.

-

Crescent Bank has a range of CD offerings with an exceptionally high APY. The shortest CD is one year, with an APY of 5.35%. The options increase by six-month increments up to three years and then go up by 12-month increments to five years. The highest APY of 5.35% is offered for 12-month and 24-month CDs. The minimum deposit is $1,000, but you won’t have to worry about maintenance fees.

-

Finally, if you don’t want to lock away a chunk of money, The State Exchange Bank offers low-commitment, high-yield options with a $1 minimum deposit. The terms are four months and seven months with a 3.00% APY or nine months with a 3.50% APY.

Compare savings accounts

The richest 1% use an advisor. Do you?

Wealthy people know that having money is not the same as being good with money. Advisor.com can help you shape your financial future and connect with expert guidance . A trusted advisor helps you make smart choices about investments, retirement savings, and tax planning.

Try it now